VAT Services for Foreign Companies and Serbian Subsidiaries

Need VAT services in Serbia? VAT registration, monthly returns, cross-border, VAT advisory, audit defense. Ex-EY, senior-only execution, fixed fees.

VAT Advisory Overview

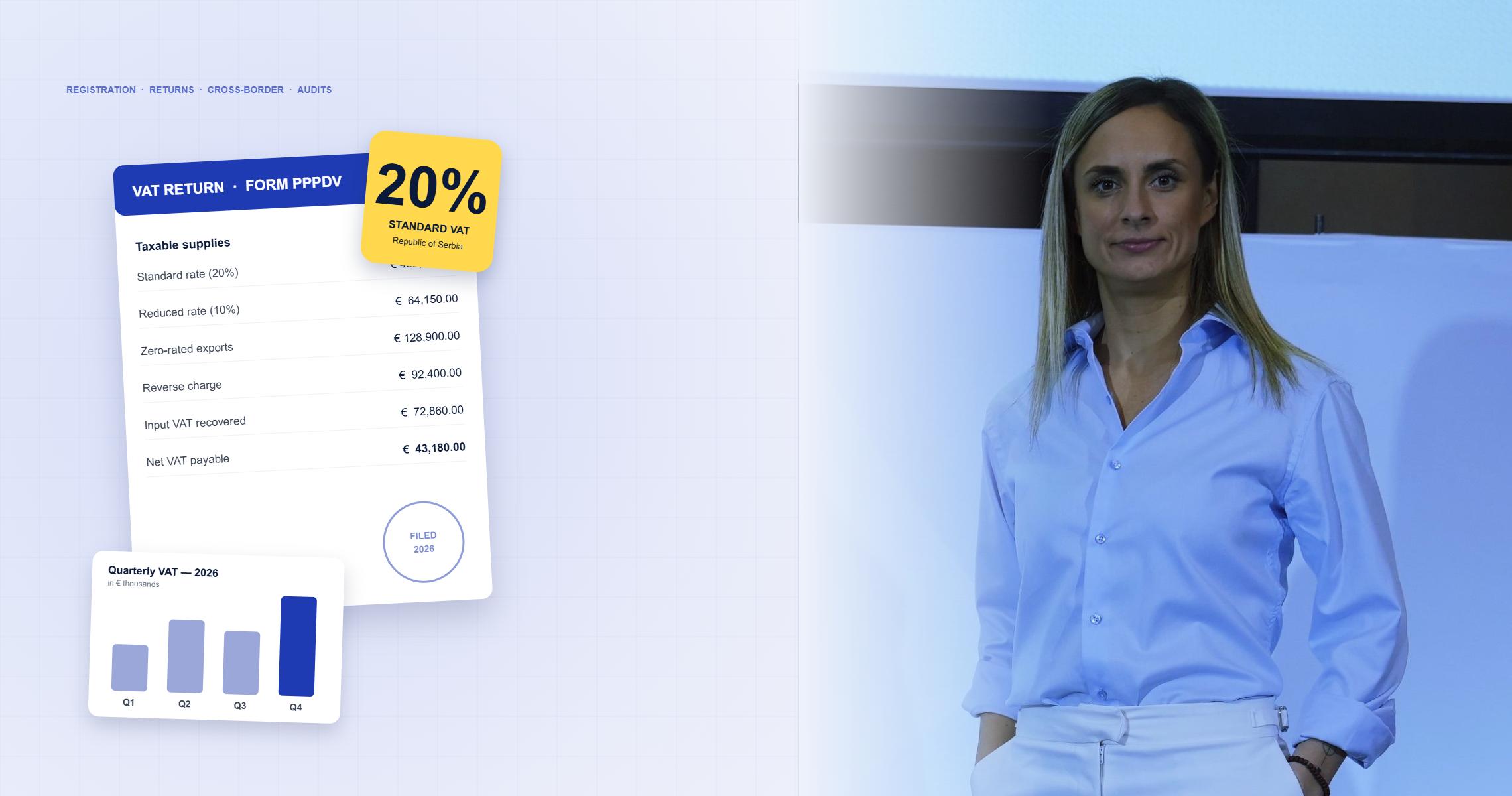

Serbian VAT looks simple - 20% standard rate, monthly electronic filings, clear thresholds. Until reverse charge on a cross-border service, non-resident registration requirements, or a tax authority query about input VAT recovery throws everything off. That's where I come in. Big Four (EY) background advising multinationals on Serbian VAT. Direct access from the first call.

How a VAT Engagement Works

Every engagement starts with a free 15-minute call. I review your situation, scope the work, and send you a clear proposal within 24 hours - defined deliverables, fixed fee, no surprise billing.

You work with me directly from first call to final delivery.

Core VAT Services

- VAT registration for foreign companies - including non-resident registration with fiscal representative

- Monthly and quarterly VAT returns - prepared, reviewed, and filed electronically

- Cross-border VAT structuring - reverse charge, place of supply, intra-group services

- Input VAT recovery - refund claims, non-resident recovery procedures, error correction

- Audit defense - tax authority queries, compliance checks, dispute resolution

- Digital services and SaaS - B2B vs B2C treatment, place of supply rules, Serbian-specific obligations

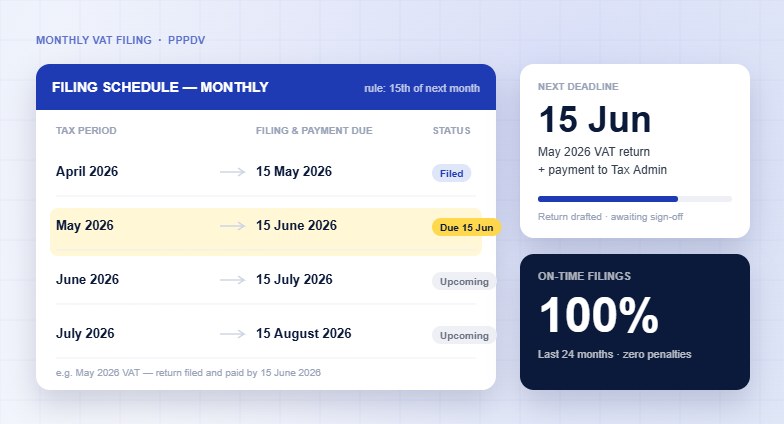

Ongoing VAT Compliance and Support

Once you're registered, I keep your VAT position compliant and efficient. Monthly or quarterly returns submitted on time, deadlines tracked, electronic filings handled. When tax authorities reach out - and they do - you have a senior advisor responding within hours, not a service ticket.

Common VAT Scenarios I Solve

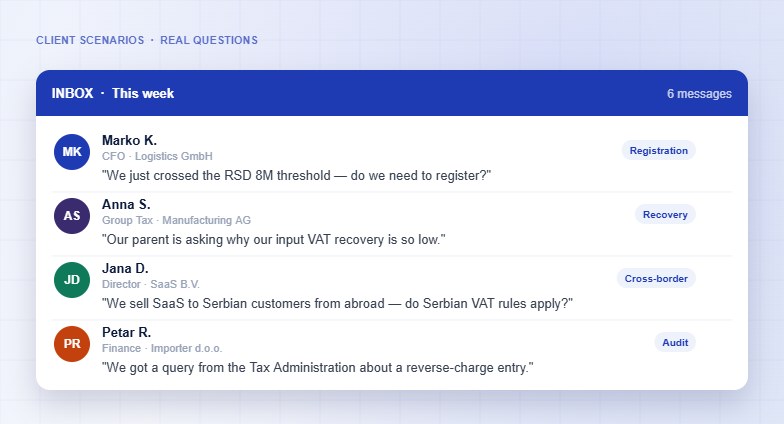

Most clients come to me with one of these:

- "We just crossed the RSD 8M threshold - do we need to register?"

- "Our parent company is asking why our input VAT recovery is so low."

- "We got a query from the Tax Administration about a reverse charge entry."

- "We sell SaaS to Serbian customers from abroad - do Serbian VAT rules apply?"

- "We're importing equipment and the customs VAT calculation looks wrong."

- "Our fiscal representative left and we need a new arrangement."

If any of these sound familiar, you're in the right place.

Serbian VAT - Common Questions

What's the VAT registration threshold in Serbia?

A foreign company must register if Serbian taxable turnover exceeds RSD 8 million in the past 12 months. Voluntary registration below the threshold is also possible - sometimes preferable for input VAT recovery.

Do I need a fiscal representative as a non-resident?

Yes. Non-resident companies registering for Serbian VAT must appoint a fiscal representative - a Serbian resident who assumes joint liability for VAT obligations. Selecting the right representative matters.

What's the Serbian VAT rate?

20% standard rate, 10% reduced rate (food, books, utilities, certain medical supplies). A few categories are exempt - exports, international transport, and specific financial services.

How often do I file VAT returns in Serbia?

Monthly for most VAT-registered companies. Quarterly filing is available for smaller taxpayers below a turnover threshold. Returns filed electronically.

Can a foreign company recover Serbian VAT?

Yes, under specific conditions and reciprocity arrangements with the foreign company's home country. Export-heavy businesses can also apply for Predominant Exporter Status for refunds in 15 days instead of 45. The procedure has strict deadlines - most rejections come from procedural errors, not substantive ones.

How does reverse charge work for cross-border services?

For B2B services received from abroad, the Serbian recipient self-accounts for VAT - declared as both output and input on the same return. Sounds neutral, but errors here trigger most of the audit queries I handle.

Do I need to use Serbia's e-invoicing system as a foreign company?

If you make B2B or B2C supplies subject to Serbian VAT, yes - Serbia's electronic invoicing system (SEF) is mandatory. Non-resident VAT-registered companies face the same obligation. Setup typically includes electronic certificate, integration with your accounting software, and proper user permissions - a common pain point for foreign companies entering the market.

Related VAT Reading

- How to get your VAT refund in 15 days instead of 45

- VAT registration in Serbia 2026 guide

- VAT exemption for export of goods - conditions and deadlines

- Year-End TP Adjustments in Serbia: A High-Stakes Customs and Tax Puzzle

.png)